The four themes behind the shift from the West to the East

May 2023 | 2 min read

The four themes behind the shift from the West to the East

While emerging markets (EM) had a challenging 2022 due to the coexistence of geopolitical risks, high inflation and supply-chain bottlenecks resulting from the Covid-19 restrictions, 2023 started off on a more favourable note.

Indeed, we believe we are at the start of a transition period, with a shift of focus from the West to the East; indeed, we are observing some positive signs which could reinforce a more constructive approach towards EM in comparison to Developed markets (DM).

In this regards, we have identified four main themes:

1. The reopening in China has been particularly positive, becoming one of the main EM growth drivers for this year. After the pandemic-related slowdown, the economic recovery is now solid and well on track, leading us to revise up our growth expectations for 2023 to 6%.

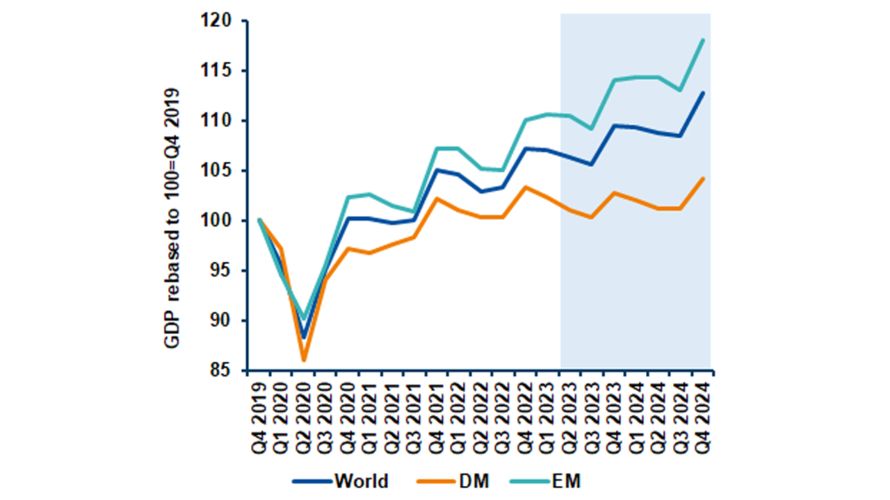

2. The earlier-than-expected reopening in China, occurred in parallel with the US economy downturn, has placed the two giants on a diverging path and contributed to a widening EM-DM growth differential, which should play in favour of the former.

3. Inflation is still high on a global level, well above central banks’ targets. However, the recent tightening of financial conditions, coupled with the banking sector turmoil, could lessen the need for aggressive rate hikes. As we have likely approached the end of the Fed tightening cycle, we expect the dollar to be stable/weaken in the second half of 2023, and this will support EM currencies.

4. Lastly, monetary tightening in many EM countries might have reached an end, placing them in an advanced stage if compared to DM. Nevertheless, while restrictive policies may be over in the majority of countries, It is important to remember that the EM landscape is still very diverse.

Having said that, we think the need to be selective in EM is high, given that the region is not homogenous. Investors should consider risks, including a stronger-than-expected tightening by the Fed, as well as geopolitical issues, such as Russia’s invasion of Ukraine and tensions over Taiwan. Lastly, we believe that higher refinancing costs, large outflows, lower liquidity and weak fundamentals might potentially lead to an increase in sovereign defaults.

DM-EM growth graph

Source: Amundi Institute. Data is as of 20 April 2023. Latest forecasts are as of 18 April 2023. EM= Emerging markets, DM= Developed markets. Shaded area refers to forecasts.

Important information

Unless otherwise stated, all information contained in this document is from Amundi Ireland Limited and is as of 11 May 2023. The views expressed in this page should not be relied upon as investment advice, a security or service recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results. Amundi Ireland Limited is authorized and regulated by the Central Bank of Ireland.

Date of first use: 11 May 2023

Doc ID: 2916632

Learn more about our Convictions

Powered by Amundi Institute